Custom Home vs. Remodel: Which Is the Better Investment for Your Property?

You’ll get the better investment when your all-in cost stays under your neighborhood’s resale ceiling while delivering the features buyers pay for. Custom home builds typically run $250–$500 per sq ft (up to $600+), take 10–16 months, and can earn a premium for modern layouts, energy performance, and smart-home readiness. Remodels often cost $150–$350 per sq ft, close faster, and track comps better—unless asbestos, soil, or change orders blow the budget. Keep going to see the 5-question test.

Custom Build vs. Remodel: Decide in 5 Questions

Where do you start when both a custom build and a remodel can raise your home’s value? Use five market tests. First, check your neighborhood’s ceiling price: if you’re already near it, remodels may protect value better than a leap to new construction. Second, evaluate lot potential and zoning; if constraints limit expansion, you’ll favor targeted upgrades. Third, compare buyer demand signals—open-plan layouts, energy performance, and smart-home readiness—then ask which path delivers them faster. Fourth, weigh customization vs. disruption: can you tolerate months off-site, or do you need phased work? Fifth, balance craftsmanship and budget by prioritizing visible, high-ROI elements such as kitchens, primary suites, and curb-impact features.

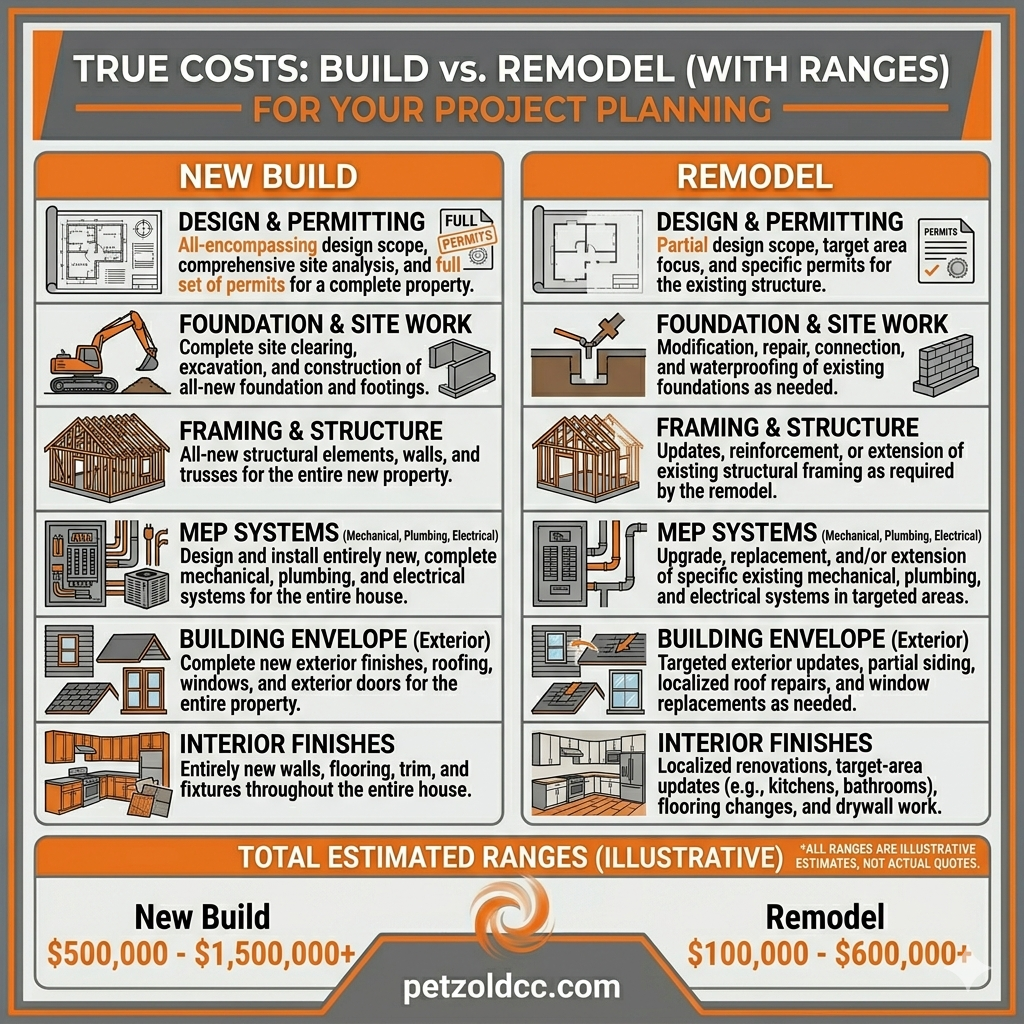

True Costs: Build vs. Remodel (With Ranges)

How much will a custom build or remodel actually cost in today’s market? National benchmarks put custom new construction around $250–$500 per square foot, with high-design or high-performance targets pushing $600+. Mid- to upscale remodels typically range from $150–$350 per square foot; kitchen-heavy or layout-changing scopes can reach $400+.

To compare options, run a cost-benefit check against your local resale comps: if your all-in build number exceeds post-build value by 10%+, you’re buying lifestyle, not equity. Remodels often pencil out better when you can keep the existing footprint, but you’ll need a tighter risk assessment to guard against scope creep and schedule drag. Price both paths with a 10–20% contingency and validate bids per trade.

What Drives Cost: Site Work, Permits, Systems

After you’ve compared headline build vs. remodel ranges, your biggest cost swings often come from site prep and utilities—grading, drainage, and new service runs can change budgets fast. You’ll also pay for permits and inspections that vary by jurisdiction and can add both fees and schedule risk. Finally, mechanical systems (HVAC, electrical, plumbing) drive major line items, and bringing them up to current code can shift ROI more than finishes.

Site Prep And Utilities

Why do site prep and utilities swing budgets so dramatically? You’re buying certainty in a highly variable scope. A flat, previously built lot may require minimal clearing, whereas sloped or fill-heavy parcels may require engineered site grading, retaining walls, and the export/import of soil. In many U.S. markets, site work typically accounts for 5%–15% of the total build cost, but complex topography or poor soils can push it past 20%, eroding ROI. Utilities add similar volatility: long service runs, rock, and groundwater raise labor and equipment time, and utility trenching costs scale with linear feet. If you’re remodeling, you often reuse existing lines, but capacity upgrades can still trigger excavation. Early surveys and subsurface scans reduce change orders and protect resale comps.

Permits And Mechanical Systems

In many markets, permits and mechanical systems quietly decide whether your custom build or remodel pencils out, because they combine hard fees with code-driven scope. You’ll see permit line items rise with valuation, added inspections, and plan-review cycles; permitting hurdles can also extend carrying costs if approvals slip weeks or months.

On the systems side, code updates often force full replacements during remodels—new panels, GFCI/AFCI protection, makeup air, duct sealing, or fire sprinklers—while new builds let you optimize layouts from day one. Mechanical zoning boosts comfort and resale appeal, but it adds dampers, controls, and commissioning. If you’re targeting high-efficiency electrification, budget for service upgrades, heat-pump sizing studies, and energy-model documentation. You’ll protect ROI by sequencing design, permit strategy, and MEP engineering early.

ROI and Resale: Build vs. Remodel

When you compare resale outcomes, you’ll often see remodels track neighborhood comps more closely, while custom builds can command a premium only if your finished home aligns with local buyer demand and price ceilings. Your ROI hinges on drivers such as layout efficiency, energy performance, and kitchens/baths, but you also face risks from over-improving, long timelines, and shifting interest-rate conditions. To choose objectively, you’ll want to model your all-in cost against realistic resale comps and a conservative time-to-sell scenario for each path.

Resale Value Comparison

How do custom builds and remodels stack up at resale once you measure return on investment instead of just sticker price? In many metros, buyers pay premiums for “like-new” efficiency, open plans, and tech integration, so a well-executed custom build can command a higher price per square foot. But resale markets also reward smart remodels that modernize kitchens, baths, and curb appeal without over-improving for the neighborhood.

You’ll often see stronger cost savings with remodels because you’re leveraging an existing structure and shortening time to market. Still, design flexibility in a custom build can translate into broader buyer appeal if you align layouts with current demand (work-from-home zones, energy performance, EV-ready garages). Compare recent comps, not averages, and price your choice against local absorption.

ROI Drivers And Risks

Why do two projects with the same budget produce wildly different ROI at resale? You’re trading on buyer demand, not construction pride. In many markets, appraisals reward finished square footage and bedroom/bath counts, so a custom build can outperform if it adds functional space, energy efficiency, and modern systems. But if you over-customize, you’ll narrow the buyer pool and discount your own features.

Remodel ROI hinges on targeting high-velocity upgrades: kitchens, primary suites, and curb appeal. Your biggest risk is hidden conditions—wiring, plumbing, and structure—that can blow the budget vs. resale equation. Track design fees, permit timelines, and carrying costs; they change break-even fast. To innovate safely, stress-test comps, cap bespoke finishes, and prioritize scalable tech (HVAC, solar-ready, smart panels).

Neighborhood Comps: Will You Over-Improve?

In many markets, neighborhood comps set a hard ceiling on what buyers will pay, so the real question is whether your custom build or remodel pushes your property beyond that range. Pull recent closed sales within 0.5 miles, match bed/bath and lot size, then calculate price-per-square-foot bands to define your likely exit value.

If your plan adds premium square footage, high-end systems, or boutique finishes without comp support, you amplify the risk of over-improvement and compress resale margins. A custom home can outperform comps only if you introduce differentiators buyers price in—energy performance, flexible layouts, ADU potential, or low-maintenance materials—while staying inside the neighborhood’s top decile. For remodels, prioritize upgrades with proven absorption: kitchens, baths, and curb-impact items that lift perceived quality without overshooting your market’s ceiling.

Financing: Custom Build vs. Remodel

Even if your plan stays within neighborhood comps, financing can still make or break the return because lenders price risk differently for new construction than for renovations. With a custom build, you’ll often use a construction-to-permanent loan: draws, inspections, and higher contingency requirements can lift carrying costs and tighten debt-to-income ratios. You can offset that by underwriting measurable upgrades—energy-efficiency packages, smart envelopes, and electrification—that reduce utility risk and support premium valuations.

For a remodel, you’ll more likely tap a cash-out refi, HELOC, or renovation loan, which may price closer to standard mortgages if the scope is defined. Your best leverage comes from targeting design trends with appraiser-visible comps and limiting structural unknowns, so the lender doesn’t haircut projected value or require reserves.

Timelines: Remodel vs. Custom Build

Because time directly affects carrying costs and resale timing, the schedule you choose can shift your total return as much as the design does. In a timeline comparison, remodels can close faster when you’re keeping the footprint and systems; many market projects run 8–20 weeks for kitchens or baths, while whole-home updates often land in the 4–9 month range, depending on scope and permitting. A custom build typically spans 10–16 months from design through punch list, with longer lead times for entitlements and procurement.

To keep velocity high, map custom vs. remodel workflows like a product roadmap: lock specs early, batch decisions, and use digital scheduling to track critical path and trade sequencing. Faster cycle time can preserve optionality for listing windows and rate shifts.

Hidden Costs: Asbestos, Soil, Change Orders

While your pro forma may assume clean demolition and predictable site conditions, hidden costs often drive the biggest gap between a “good deal” and a disappointing ROI. In remodels, asbestos abatement can add five figures and trigger permitting delays; you’ll also pay for testing, containment, and specialized disposal. On the site side, soil issues like expansive clay, undocumented fill, or high groundwater can force engineered foundations, drainage redesigns, and export/import hauling—line items that rarely show up in early comps. The other silent multiplier is change orders: once walls open or crews hit unforeseen conditions, scope creep converts fixed bids into time-and-material totals. You’ll protect margin by budgeting a realistic contingency, requiring unit-rate pricing, and using 3D scanning or geotech data to reduce uncertainty.

When a Custom Build Wins Financially

When does a custom build beat a remodel on ROI? You’ll see it when your existing structure can’t support high-value upgrades, or when local comps reward modern layouts, energy performance, and smart-home systems. If you’re in a market where new builds sell at a clear premium per square foot, a custom build can price in that premium from day one. You also reduce uncertainty: you won’t sink capital into hidden constraints that cap appraisal value. Your pro forma improves when you can optimize floor-plan efficiency, add rentable space (ADU, basement suite), and meet current code without costly retrofits. Remodel ROI often compresses when you’re chasing functional obsolescence rather than adding net-new utility buyers pay for. You’re investing in controllable value drivers.

Frequently Asked Questions

Will a Remodel Void My Home’s Existing Warranties or Insurance Coverage?

Yes, a remodel can void or limit warranties and trigger insurance changes if you don’t manage approvals and documentation. Like a circuit you reroute, one cut can dim protections elsewhere. Manufacturer and contractor terms often exclude modified installations—surprising warranty implications. Insurers may re-rate risk, require permits, or deny unreported upgrades, creating insurance coverage gaps. You’ll protect value by notifying your carrier early, using licensed trades, and keeping inspection records.

Can I Live in the House During the Remodel?

Yes, you can often live in the house during a remodel, but it depends on the scope, safety, and permits. If you’re working in kitchens, baths, HVAC, or electrical systems, plan phased work or temporary utilities. Track living costs: short-term rentals can outpace the costs of lost productivity and delays. Confirm zoning rules and occupancy requirements for temporary kitchens, trailers, or added bathrooms. You’ll reduce risk by isolating dust and scheduling high-impact trades strategically.

How Do I Choose Between an Architect and a Design-Build Firm?

Choose an architect when you need maximum customization, competitive bidding, and tighter control over design intent; prioritize Architect selection by reviewing comparable projects, fee structure, and coordination track record. Choose a design-build firm when speed, cost predictability, and single-point accountability matter most; design-build pros include integrated estimating, fewer change orders, and faster schedules. Benchmark both with ROM budgets, schedule guarantees, and post-occupancy performance data in your local market.

What Tax Implications Differ Between Building New and Remodeling?

New builds and remodels trigger different tax treatments: new builds usually capitalize costs into basis, while remodels may unlock targeted tax credits and faster write-offs. IRS data show home-improvement spending topped $500B in 2023, making these differences material. With a remodel, you may deduct some repairs now and apply depreciation rules for rental/office components. With new construction, depreciation typically starts when placed in service, and credits hinge on energy standards.

How Do HOAs Affect Approvals for a Custom Build or Major Remodel?

HOAs can substantially shape your custom build or major remodel by enforcing HOA restrictions and controlling the approval process. You’ll submit architectural plans, materials specs, and timelines; review cycles often add 30–90+ days, impacting carrying costs and contractor pricing. You can face height limits, setbacks, façade, solar, and landscaping constraints, reducing design flexibility. You’ll protect schedules by pre-consulting the committee and aligning drawings to covenants upfront.

Conclusion

If you’ve priced a remodel and a custom build in the same quarter, you’ve probably noticed the coincidence: their totals can converge once you add site work, permits, and system upgrades. Your better investment depends on comps—if nearby sales cap value, a higher-spec build won’t pencil. If land value dominates and layout limits remain, a custom build can more reliably lift resale. Either way, tighter scopes, fewer change orders, and realistic timelines protect ROI.